Solid buffers soften energy blow to EM Asia

While Mongolia is fragile, Malaysia, Thailand, Vietnam, Indonesia, the Philippines, and China are resilient to sovereign stress.

The sovereign risk picture across East Asia & Pacific in 2026 is defined by the Hormuz-related oil supply shock that is feeding into current account deterioration amid government revenue mobilization pressures. Yet all but one of this region’s sample countries perform better on macro-fiscal sovereign risk indicators than most of their broad emerging and frontier market peers, making them somewhat of an EM safe haven. As with the broader EM universe, EAPAC sovereigns are benefiting from resilient global appetite for risk assets. While VIX rose in March in response to the U.S.-Israel war with Iran, volatility has remained subdued compared to 2025’s tariff reaction. Certainly, this year’s benign global investor sentiment is a mechanical tailwind that eases sovereign strains throughout EM.

However, the scale of fuel shortages across EAPAC and the reduced growth outlook globally have exacerbated sovereign risks in these countries. Mongolia is experiencing widespread gasoline and diesel shortages and has less than 30 days of inventory. The Philippines has declared a national emergency amid gasoline station closures and airlines rationing jet fuel. In Indonesia, local shortages have led the government to introduce limited subsidies for fuel purchases and asked civil servants to work from home. Vietnam’s aviation sector is experiencing a major jet fuel shortage, resulting in domestic flight cancellations. Malaysian refineries have slashed production given limited crude stocks. China is coping thanks to its enormous oil reserves and increased domestic production, although it has curbed some of its fuel exports.

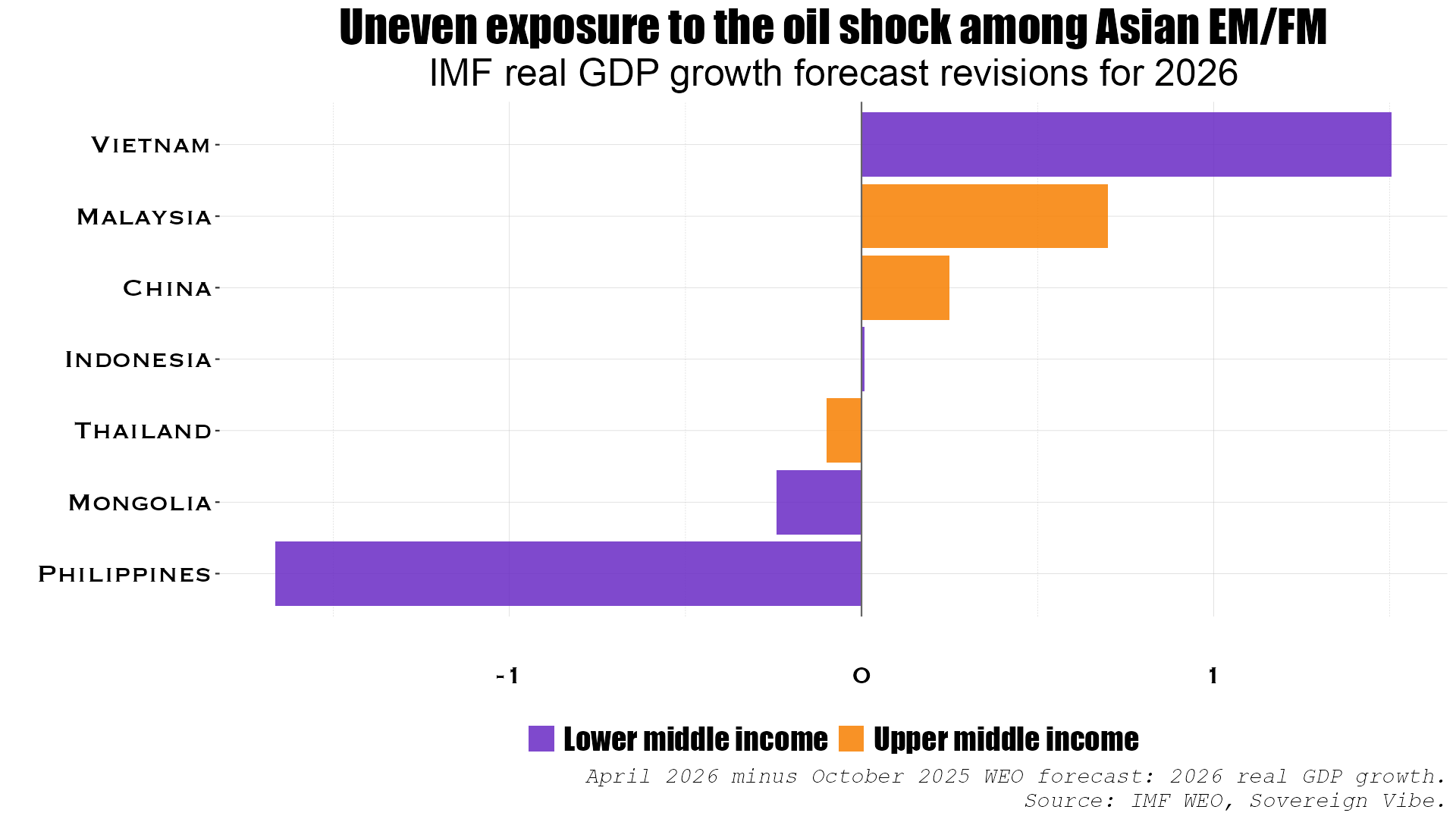

Due to the severe disruptions from the Middle East conflict, the IMF has made a significant downward revision to its forecast for 2026 growth in the Philippines and, to a lesser extent, in Mongolia and Thailand. Dampened global demand is threatening sources of hard currency inflows, whether from Mongolian mineral exports, tourism in the Philippines, and Thailand, and remittance flows more broadly. In addition to the war shock, the Philippines is also experiencing high inflation, a sharp decline in public investment, and dampened investor confidence due to a flood-related corruption scandal.

While output in the region’s other countries is also at risk from the Hormuz closure, Malaysia is displaying resilient domestic strength amid tech-driven growth prospects, and Vietnam continues to benefit from structural reform, foreign direct investment, and free trade agreements. In China, state-led innovation in AI and biotechnology are offsetting a growing crisis in its property market.

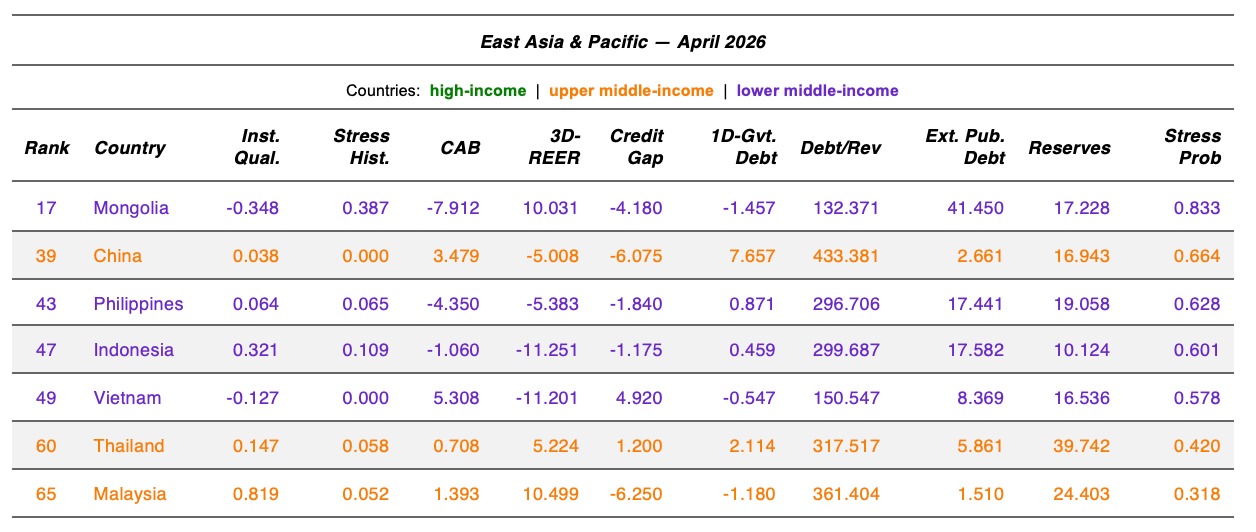

Against this challenging backdrop, sound economic policies and credibility are helping to insulate much of the region from the ongoing energy supply disruption. Almost all countries in the region have significant international reserves as a share of GDP, which help protect against balance of payments crises. Only Indonesia and Mongolia likely require more of an FX buffer. Current account balances are mostly positive, with Mongolia and the Philippines exhibiting the only sizable deficits, and no country other than Mongolia exhibits are oversized external public debt burden.

Moreover, three-year real exchange rate depreciation is reducing sovereign risks in Indonesia, Vietnam, the Philippines, and China, though appreciation is a source of concern in Malaysia, Mongolia, and, to a lesser extent, Thailand. On the fiscal front, Mongolia, Malaysia, and Vietnam are all reducing their government debt burdens, and the only worryingly large increase is in China. Similarly, public debt-to-revenue ratios are comparatively low in Mongolia and Vietnam, with Indonesia and Vietnam making improvements on this metric. China, Malaysia, and Thailand all exhibit large debt-to-revenue readings but have the institutions and reserve cushions to manage the associated sovereign risks.

Mongolia stands apart as the region’s clear sovereign stress outlier. At 83.3% probability and ranked 17th globally, it combines a very wide current account deficit (-7.9% of GDP, 91st at-risk percentile), a large external public debt stock (41.5% of GDP, 90th percentile), and real exchange rate appreciation into a fragile external position. China’s risk profile is shaped by a different set of dynamics: a debt-to-revenue ratio of 433 (87th percentile) and one of the fastest rates of government debt accumulation in the sample (91st percentile) keep its stress probability at 66.4%, despite a robust current account surplus and negligible external public debt—an unusual combination that speaks to China’s unique position in the world economy. Vietnam, while benefiting from a strong external position, carries the region’s most acute private credit vulnerability: a credit gap at the 97th percentile flags the risk of excessive private sector leverage that could spill over into sovereign stress. Thailand and Malaysia anchor the region’s low-risk end, with Thailand’s vast international reserves (39.7% of GDP) and Malaysia’s institutional quality acting as powerful buffers against stress.

Exhibit 1

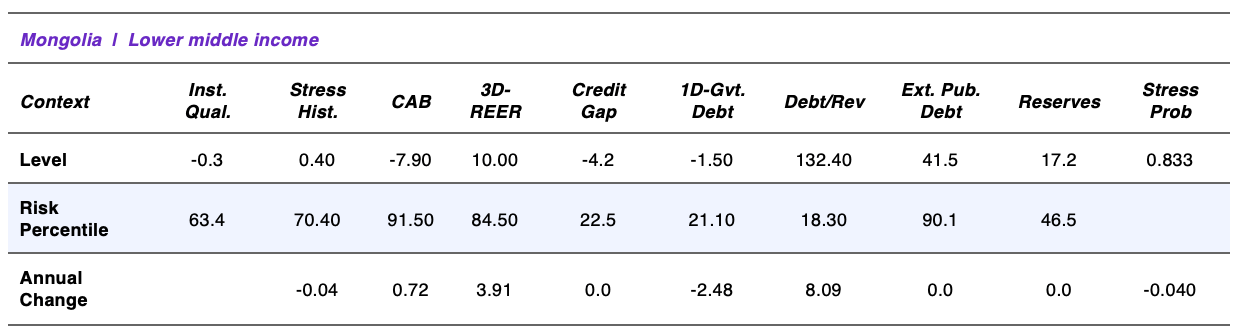

The table below presents regional countries and their data points across the ten independent variables that predict sovereign stress probability and the dependent variable of sovereign stress itself. This analysis uses data from international databases, usually in yearly format. As such, there may be discrepancies with national sources and/or higher-frequency premium data sources. Such divergences may also arise because when actual or forecast data is unavailable for the reference year, data from the previous period is pulled forward.

For some indicators such as external public debt, data may be partial (e,g, SOE debt may not be included) or wholly missing from official databases depending on government reporting. Using official databases enables fairness in cross-country comparisons, and better granularity is more easily achievable in country-specific deep-dives.

Exhibit 2

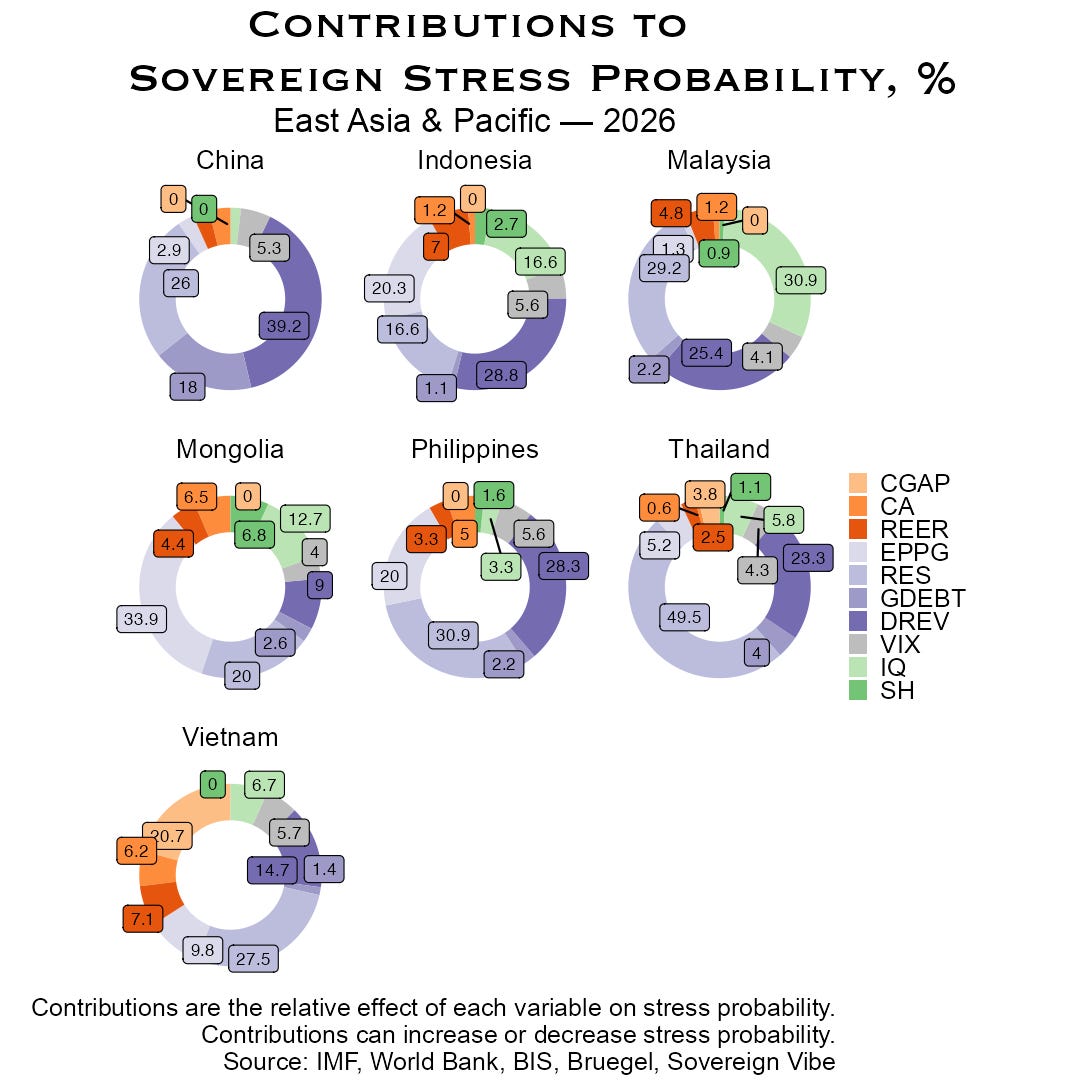

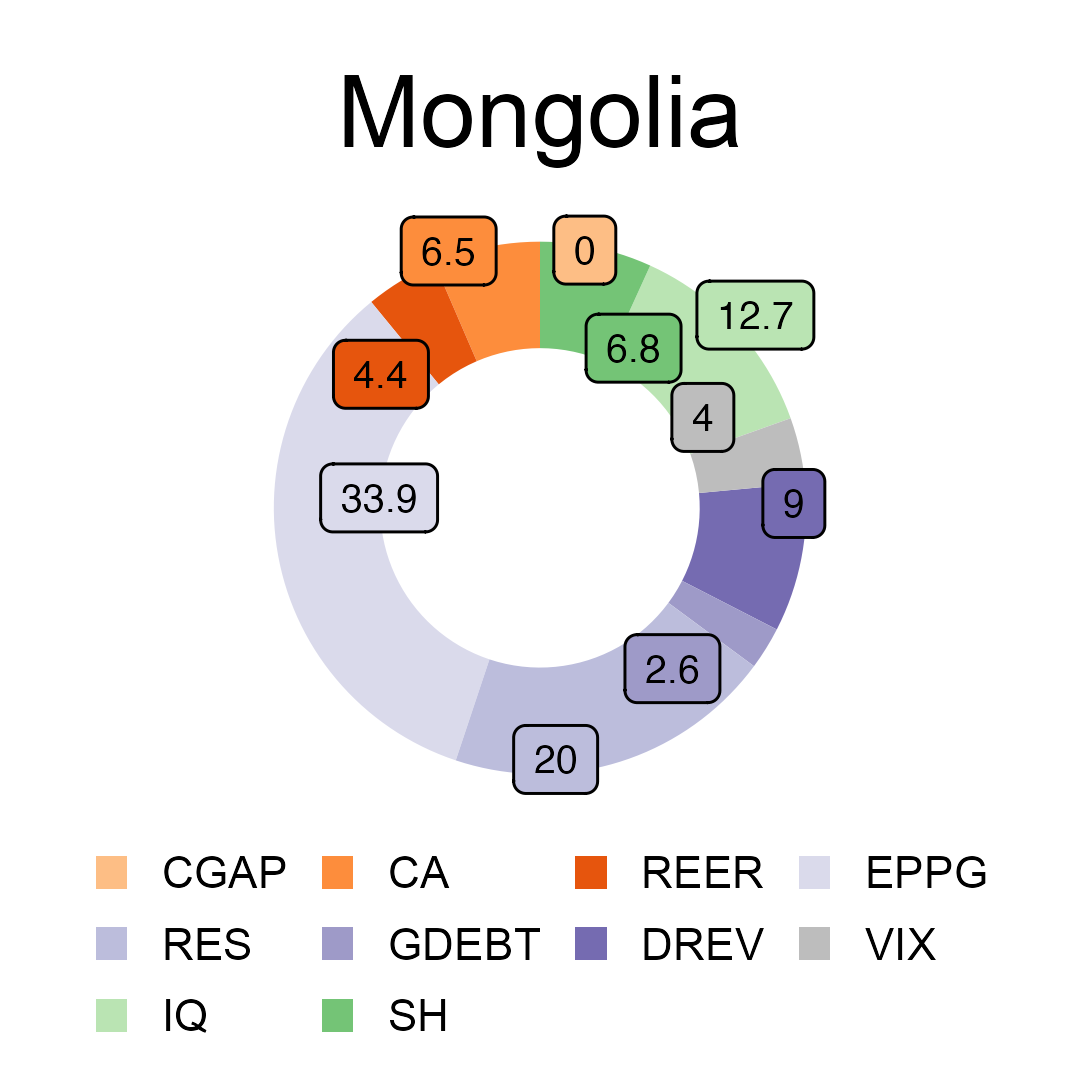

Each ring plots the absolute contribution of the ten model inputs to each country’s probability of sovereign stress. This is calculated as each coefficient-variable product’s percentage of the 10 pairings’ linearly-combined sum.

Mongolia

For Mongolia, external public debt, international reserves, and institutional quality are the largest contributors to the country’s sovereign risk profile.

External Public Debt: At 41.5% of GDP, Mongolia’s external public debt sits at the 90th at-risk percentile—one of the highest in the global EM sample—reflecting heavy reliance on external financing and the associated currency and refinancing risks.

International Reserves / GDP: At 17.2% of GDP (46th at-risk percentile), Mongolia’s international reserve coverage is the second-largest contributor to its model-estimated stress profile. While not acutely depleted, this level of reserves covers less than half its external public debt burden and is also small in comparison to the country’s yawning current account deficit (-7.9% / GDP).

Mongolia’s external vulnerabilities are the most severe in the EAPAC sample and rank near the top of the global at-risk distribution. Three-year real exchange rate appreciation of 10.0 percentage points (84th percentile) compounds the competitiveness challenge, narrowing the path to external rebalancing. Partially offsetting these pressures, negative government debt growth (21st percentile) and the low debt-to-revenue ratio (18th percentile) reflect conservative fiscal policy.

Mongolia’s model-estimated probability of experiencing sovereign stress in the near-term stands at 83.3%, ranking it 17th out of the 72 in-sample countries in 2026.

Mongolia’s sovereign risk profile is improving in 2026, with stress probability declining 4 points, the 40th-largest improvement in the sample.

Accelerating real exchange rate appreciation (3yr REER Δ +3.9pp, rising to +10.0pp) and a rising public debt-to-revenue ratio (Δ +8.1, from 124.3 to 132.4) are the primary risk-increasing forces in 2026 relative to last year.

Government debt growth shifted from slight expansion to contraction (Δ −2.5pp of GDP, from +1.0pp to −1.5pp) and the current account deficit narrowed modestly (Δ +0.7pp of GDP to −7.9%); a declining stress history (Δ −0.043) adds a further mitigating signal, while the global VIX decline is a major mechanical driver of Mongolia’s improvement.

The report continues for paid subscribers below.

Keep reading with a 7-day free trial

Subscribe to Sovereign Vibe to keep reading this post and get 7 days of free access to the full post archives.